Investors often hear of the significant difficulties in ramping up industrial manufacturing processes, such as for automobiles or wind turbines. But the most challenging scale up might occur in biopharma and industrial biotech.

It took decades of research and contributions from hundreds of scientists, but by July 2017 Spark Therapeutics was ready to submit the biologics license application (BLA) for voretigene neparvovec. The regulatory submission for the experimental therapy, an adeno-associated virus (AAV) gene therapy capable of improving vision in patients with a rare eye disease, was roughly 60,000 pages long. It might be surprising to learn clinical data represented only a small portion of the information. Indeed, data related to chemistry, manufacturing, and controls (CMC) of the AAV vector and genetic material comprised most of the application.

The total final scale of the biomanufacturing process: roughly 400 liters.

To be sure, an AAV gene therapy product might be the most difficult therapeutic to manufacture. The U.S. Food and Drug Administration (FDA) places stringent controls on the science, engineering, and manufacturing of therapeutic biologics. Venture capitalists and entrepreneurs often point to the lack of similar barriers for industrial biotech processes, which have the potential to manufacture materials and ingredients ranging from fuels to foods, enzymes to commodity ingredients directly competing with established petrochemical processes. One day we may even use microbes to synthesize metallic nanoparticles for solid-state batteries powering electric vehicles.

But what industrial biotech lacks in regulatory scrutiny it pays for many times over in physical constraints and economic headaches.

The inability to reproducibly and economically scale biology remains a significant bottleneck holding back the field of synthetic biology. Making it easier to tinker with genetics provides some relief, but a longitudinal view of developments to date and deeper understanding of bioprocess scale-up shows how the same roadblocks are still keeping ingredients from reaching market. An exceedingly small amount of capital and number of entrepreneurs are paying attention.

Need more finch? Here's our newsletter.

Welcome to The Voyage!

Oops! Something went wrong while submitting the form.

Mother Nature Doesn't Give Out Participation Trophies

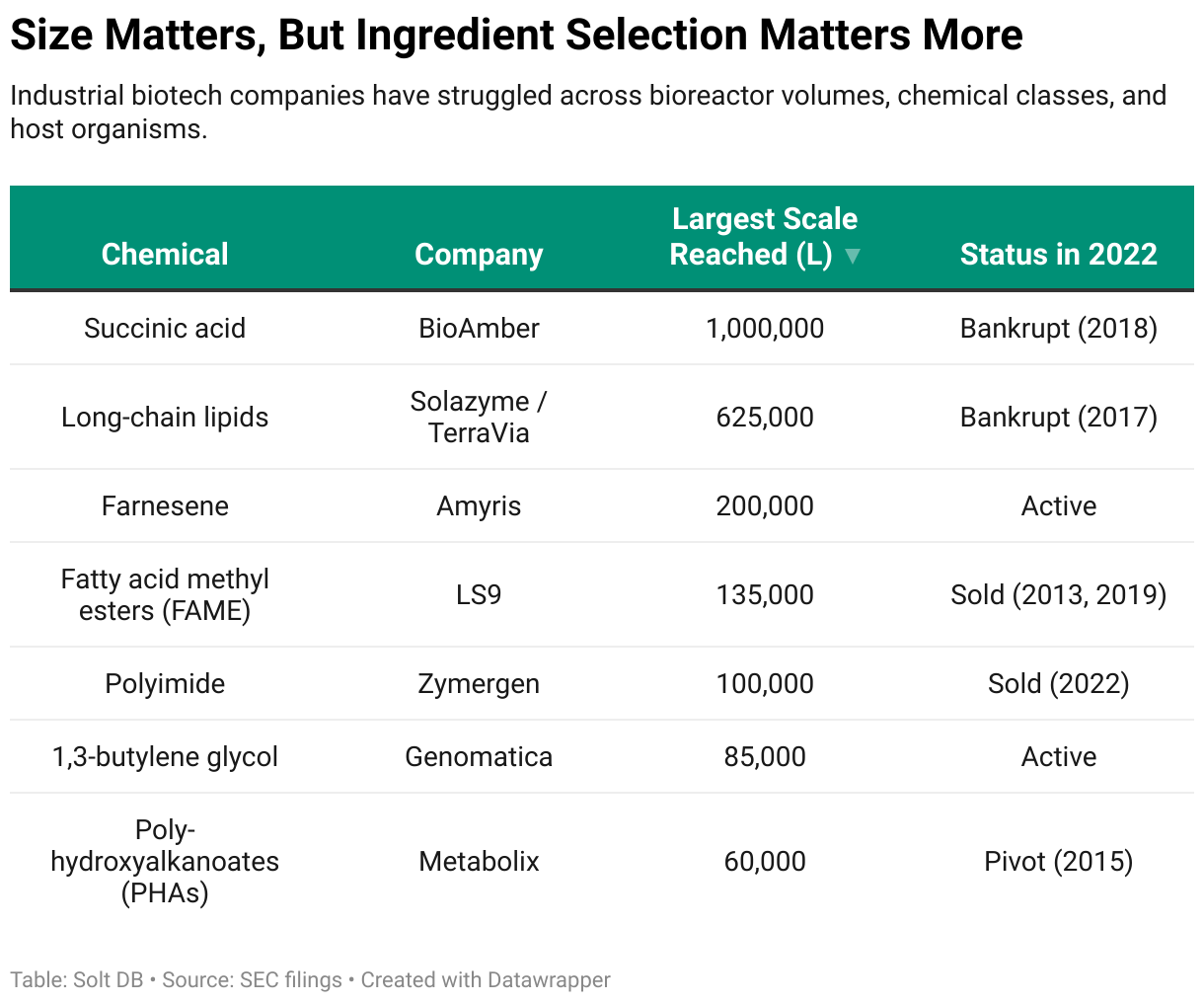

The definition of "commercial scale" varies widely across industries. Whereas commercial bioprocesses in biopharma (gene therapy, cell therapy, antibodies, mRNA, and so on) typically reach a ceiling near 2,000 liter (L) volumes, an industrial bioprocess can reach over 1,000,000 L depending on the host organism and ingredient.

Despite the larger volumes of industrial biotech relative to biopharma, Mother Nature doesn't guarantee economies of scale just for showing up.

The primary technical goal during development is to optimize three metrics:

Titer (g/L) is the concentration of product within the bioreactor (mass per unit volume). This is the most important metric in determining bioreactor volume requirements and product output for a commercial bioprocess, from which most economic calculations are derived.

Productivity (mg/L/hr) is the rate at which the microbe creates the product (mass per unit volume per time). Productivity primarily determines the number of production runs achievable in a given amount of time, which also impacts product output.

Yield (%) is the ratio of feedstock required to create a certain amount of product (mass per mass = g of carbon in / g of carbon out). Although the maximum theoretical yield can never be achieved because a cell requires carbon for growth and maintenance energy, yield can be improved by reducing the creation of byproducts.

Bioprocess optimization takes place across multiple step changes in scale:

Lab scale typically involves benchtop microbioreactors (3 mL = 0.003 L), shake flasks and minibioreactors (250 mL = 0.25 L), and multi-liter vessels up to 10 L.

Pilot scale typically encompasses multi-hundred liter to 1,000 L bioreactors, although French energy supermajor Total once deployed a 10,000 liter bioreactor in a pilot-scale facility attempting to make jet fuel.

Demonstration scale encompasses bioreactors between 10,000 L and 150,000 L volumes. The capacity required depends on the ingredient being manufactured.

Commercial scale can vary widely based on the host organism and process conditions, but typically require bioreactors of at least 100,000 L and all the way up to 1,000,000 L.

What does this mean in a practical sense?

One common analogy likens a microbial cell to a factory. The factory takes an input and manipulates it in reproducible steps along an assembly line. The input is carbon (typically a sugar or carbon gas) and the assembly line is a metabolic pathway, with each step represented by an enzyme that transforms the carbon-based molecule into something slightly different. Stitch together just enough enzymes in just the right order and you can produce a meaningful, and hopefully valuable, ingredient.

The field of synthetic biology has been primarily focused on addressing previous bottlenecks, namely increasing experimental throughput and data interpretation. In other words, how many possible iterations of a metabolic pathway can be designed, built, and tested for maximizing output of a desired product.

If many designs can be measured, then it increases the chances of stumbling upon a metabolic pathway with improved titer, productivity, and yield. If those metrics can be improved, then it increases the chances of developing an economically viable commercial-scale bioprocess.

This is a brute force approach. In the distant future it might be replaced by computational modeling of metabolic pathways and individual enzymes, designing cells in silico, and then synthesizing entire cells to exacting specifications from synthetic DNA.

Until then, the brute force approach will have to do. It's valuable. It significantly expands the amount of biochemical space that can be accessed with our limited understanding of biology, but it doesn't completely address the bottlenecks in bioprocess scale-up that continue to hinder industrial biotech.

What's Old Is New Again

Whether the calendar reads 2009 or 2022, two bottlenecks have crushed company after company in industrial biotech:

overall process economics, including feedstock costs and downstream purification steps

translational limitations from lab scale to commercial scale

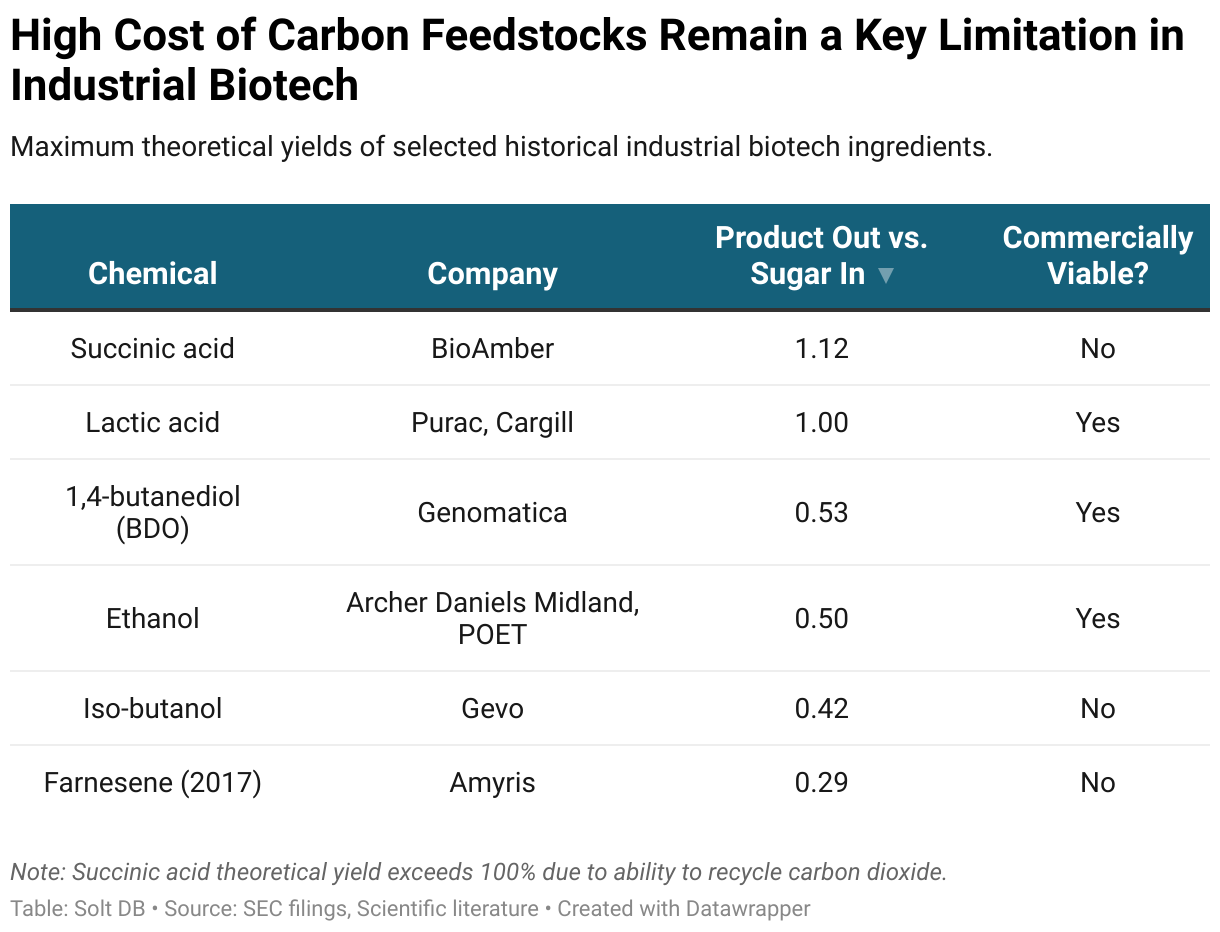

The high cost of carbon feedstocks is mostly out of the control of high-throughput foundries and cloud labs. Tinkering with genetics can greatly improve yields, but maximum theoretical yields are largely determined by product selection at the outset. If the metabolic pathway for creating a commodity chemical requires too much sugar relative to product output, then the odds of creating an economically viable commercial-scale bioprocess are low.

Consider the maximum theoretical yields (expressed as mass of product created per mass of sugar fed) for several common ingredients targeted by industrial biotech companies to date:

And although biomanufacturing is downstream of foundries and cloud labs, purification and product recovery steps are downstream of biomanufacturing. It helps to draw a big circle around "commercial process" to include the mundane mechanical and chemistry aspects, too.

To hammer home the point again, bioprocesses don't automatically earn economies of scale. Poor process economics cannot be solved by increasing the volume of the commercial-scale bioreactor. That can actually make the economics worse. Ingredient selection is paramount. Just because nature can make an ingredient doesn't mean a company can produce it at scale for a profit – even if they leveraged high-throughput techniques during development.

Consider several common ingredients targeted by industrial biotech companies to date:

The competition to create bio-based BDO provides a good case study illustrating the points above.

The agricultural biosciences company now known as Yield10 Biosciences was formerly an industrial biotech pioneer known as Metabolix. The company's initial focus was polyhydroxyalkanoates (PHAs), a group of natural chemicals that share properties with polyesters. The goal was to convert PHAs into more valuable chemicals, including BDO. The first industrial microbe was finalized in 2009, and fermentation runs in 60,000 L bioreactors were completed in 2010. Yet by 2014 the company could only muster 275 metric tons (MT) of the precursor ingredient per year across its pilot-scale footprint.

BioAmber was developing bioprocesses for producing biosuccinic acid, which would be used as an intermediary to manufacture tetrahydrofuran (THF) and BDO. It conducted multiple fermentation runs in bioreactors exceeding volumes of 1,000,000 L in 2017, and could recycle carbon dioxide in the metabolic pathway. The company's first facility had a nameplate capacity of only 30,000 MT of succinic acid per year, but would still require 0.4% of North American sugar output. That's an incredible amount for a single, small facility. The business was liquidated by the end of 2018.

Genomatica eventually developed a bioprocess for creating BDO directly from sugar, eliminating the need to create intermediates such as succinic acid and PHAs. Bioprocess optimization and scale-up wasn't quick or easy. The company's BDO titer went from 15 g/L in January 2009 to 144 g/L in April 2016. The bioprocess was licensed to Novamont, which operates a 30,000 MT per year facility in Italy. A second facility of 65,000 MT per year is being constructed in Iowa by Qore, a joint venture between Cargill and HELM, and should be operational by 2024.

The market for more sustainable chemicals is driving adoption, but economics could still have the last say. Global petroleum-based BDO production capacity is estimated at 4 million MT per year, but global demand for BDO is only 2.5 million MT per year. That's not a typo.

Nonetheless, as the development of bio-based BDO demonstrates, the world's most successful industrial biotech companies – Genomatica, Covation Biomaterials, DSM, Novozymes, Cargill – have achieved success through proper ingredient selection, rigorous engineering, an abundance of patience, and vertical integration of the technology stack from lab to commercial scale. The last part has been key for determining the haves and have nots.

The second major bottleneck hampering bioprocess optimization and scale-up is the inability to translate lab-scale experiments to commercial-scale processes. This is the primary limitation hanging over high-throughput foundries and cloud labs.

Put another way, the conditions that exist at 250 mL are quite different from those at 100,000 L. Although volume scales linearly (100 L to 100,000 L is an increase of 1,000x), many other metrics scale in a non-linear relationship. Heat transfer, mixing, osmotic pressure, the shearing force placed on cells, and the accumulation of mutations within the seed train all present unique challenges.

It's interesting to note that translating lab-scale experiments to commercial-scale processes is a challenge even within the biopharma industry, which rarely needs to exceed 2,000 L volumes. Industrial bioprocesses reaching 150,000 L or more usher in a whole new world of pain.

That's not to say the field is devoid of progress. One fantastic development has been the introduction of the ambr 250 system by TAP Biosystems, which was acquired by Sartorius. Each system is a series of up to 12 minibioreactors measuring 250 mL each that can be run in parallel. Finely-tuned sensors can measure bioprocess metrics and handle feeding, enabling the reproducible and high-throughput experimentation craved by synthetic biologists. These systems were not readily available to or widely used by earlier industrial biotech companies such as Metabolix, BioAmber, LS9, and Solazyme.

ambr 250s cannot exactly replicate the conditions of a commercial-scale bioreactor, nor for every host organism or metabolic pathway, but they're generally considered a state-of-the-art tool for bioprocess optimization and scale up.

Some scientists still question the value-add.

One hurdle is the economics of ambr 250s themselves. Each system costs up to $1 million, has a 12- to 24-month wait time, and eats up over $100,000 in annual operating costs. The disposable, single-use bioreactor vessels cost about $1,000 each. The high costs of minibioreactors, including ambr competitors, make the tools largely inaccessible to startups and potentially difficult to justify for most industrial biotech ingredients.

It's telling that whereas some companies have gone all-in on ambr 250s, several industrial biotech leaders have taken a more cautious approach. The results for those who threw down millions in venture capital funds have been mixed at best.

Ginkgo Bioworks owns a staggering amount of the ambr 250s that have ever been manufactured. However, it largely avoids downstream process development and has struggled to deliver commercially viable strains to customers. The company's foundries delivered an operating loss of $187 million in the first nine months of 2022.

Zymergen owned ambr 250s, built an impressive high-throughput experiment platform complete with software tools such as Orion, and touted its "biofacturing" platform. Quantities of Hyaline, the company's first product, shipped to customers for validation were sourced from third parties and not even manufactured using fermentation.

Amyris owns a vertically integrated technology stack and has manufactured multiple ingredients in 200,000 L bioreactors, but has struggled to manufacture ingredients profitably. The company has not generated positive product gross margin since the second quarter of 2021, although that's mostly due to ramping new consumer brands.

Therein lies one of the many nuances of the field. One of the most valuable uses of ambr 250 systems in industrial biotech is not scale up, but scale down. Already-scaled companies such as Bolt Threads or Genomatica can toss industrial strains into minibioreactors (or pay foundries and cloud labs to do so) armed with the rare knowledge of how the process behaves at commercial scale, optimize it further, and then hopefully scale it back up with improved economics.

The caveat is there aren't many of these ingredients for foundries and cloud labs to tap into, while the already-scaled companies get to dictate financial terms for (re)development work. These deals can still be a win-win, but they alone won't be enough to keep the lights on and the robots running.

Don't Make Manufacturing Hell Eternal Damnation

As the field of synthetic biology races ahead, it would be wise for investors and entrepreneurs to consider the historical difficulty in bioprocess optimization and scale-up. Industrial biotech companies have failed for many reasons, but the inability to create economically viable commercial-scale bioprocesses is often a driving factor. The most important bottlenecks largely remain unaddressed as 2023 approaches.

Although high-throughput experiment platforms can make meaningful contributions to the optimization of metrics such as titer and yield, there's more to enabling successful commercial products than tinkering with genetics. Note that this article didn't even address the need to solve customer pain points, or navigate supply chain and distribution logistics, or right-size a company's cost structure.

Nonetheless, the primary problem for industrial biotech is not a lack of capacity. There are several market research reports, and now even an executive order from the White House, proclaiming the need for more "precision fermentation" capacity. It certainly wouldn't hurt. It certainly would be wise to start developing policy frameworks and incentives. But we won't get very far merely throwing more steel in the ground and a neon sign in the window saying we're open for business.

Companies and venture capitalists can say whatever they want to raise money and tout new funds. Just remember Mother Nature doesn't hand out participation trophies, and the market wields a sledgehammer and takes no prisoners.

Yes, biotech stocks can beat the market.

Solt DB is a biotech equities research firm. We manage a real-money, long-term oriented, 100% transparent investment portfolio called Finch Trades. As of June 30, 2026 (updated quarterly), we're outperforming the S&P 500 by 97.7%, Nasdaq 100 by 83.7%, XBI by 60.5%, and Ark Genomic Revolution ETF by 64.4%.

Memberships to investment research fund our mission as a public benefit company and keep us fiercely independent – so we can keep giving tech bros the bird. No ads, no clickbait, no hype. Join today for $26.25 per month.

.svg)

.svg)

.svg)

%20(squoosh).jpg)

%20(squoosh).jpg)

.svg)

.svg)

.svg)