Sometimes the biggest problems have the simplest solutions. For Novo Nordisk, reigniting the growth engine means unleashing the RNAi platform it acquired in December 2021.

London faced a looming crisis in 1894. The city was struggling to keep its streets clean and clear of the primary transportation pollutant at the time: horse manure.

An article published in the Times of London estimated that in half a century every city street would be under nine feet of horse shit. By then, where else could they put it? Horses, the primary mode of transportation, would be the undoing of one of the world's greatest cities. It was a problem with no solution.

Until, you know, cars were invented. We traded horse manure pollution that needed constant removal for a bunch of invisible gases that effortlessly float away. Now that's progress. We'll never be undone by transportation pollutants again...

Unfortunately, the Great Horse Manure Crisis of 1894 didn't actually happen. It's the name of an article that published the fictitious story in 2004. The term is used as an analogy for describing times when everyone panics over seemingly intractable problems that might be solved by simply looking at them from new perspectives. That might include adopting new technologies that aren't currently part of the conversation.

Novo Nordisk is a great example. Although the stock chart does resemble a steaming pile of horse manure, the debate over the proper strategic direction of the business sure looks like a Great Horse Manure Crisis of 1894. Everyone is talking about all the horse shit piling up in the city streets, which has put management on the defensive. Executives are too focused on salvaging obesity or creating favorable comparisons to Eli Lilly, a peer too diversified for the Danish pharma giant to realistically catch. The pipeline is too heavily invested in cardiometabolic disorders. Throwing more money at share buybacks won't help much. It's already repurchased $26.3 billion in stock in the last decade. The current strategy is unlikely to be effective whether it's 2026 or 2036.

Instead, management should acknowledge that the horse manure does indeed need cleaned up, but decouple the growth narrative from the cutthroat obesity landscape. Novo Nordisk already acquired the solution to its problem 48 months ago.

In December 2021, the pharma giant spent $3.3 billion to acquire Dicerna Pharmaceuticals, which developed one of the leading RNA interference (RNAi) platforms. Despite emerging as a must-have therapeutic modality -- including for next-generation obesity assets that might avoid the problems of GLP-1 agonists -- Novo Nordisk has curiously handicapped its internal tools.

It's time for the new strategy team led by Hong Chow to unleash the power of RNAi on the investment narrative.

Need more finch? Here's our newsletter.

Welcome to The Voyage!

Oops! Something went wrong while submitting the form.

Genetic Medicines Might Be the Future of Obesity Treatment

RNAi is having a moment. Novo Nordisk, which owns a top 3 RNAi platform, is somehow on the outside looking in.

Companies have demonstrated promising results across a range of diseases and tissue types, targeting gene expression in the liver, fat, muscle, brain, and lungs. That includes crossing the blood-brain barrier with subcutaneous dosing, something no other genetic medicine can do, to potentially treat Parkinson's disease or Alzheimer's with two to four doses per year. RNAi can be formulated for a nebulizer, which means it can be inhaled to potentially treat inflammatory lung diseases like asthma. The first ever bispecific (dimer) RNAi candidate recently started a phase 1 clinical trial. It silences two cardiovascular targets, PCSK9 (for reducing cholesterol) and ApoC3 (for reducing triglycerides), which might represent a paradigm shift in how we treat and prevent cardiovascular disease. Drugs that inhibit either of those two targets collectively generated full-year 2025 revenue of over $4 billion with a peak far over the horizon.

Meanwhile, several next-generation obesity targets are uniquely suited for RNAi. That includes INHBE (expressed in the liver) and ALK7 (expressed in fat tissues), which have written exciting new narratives for other drug developers. Discovered only recently through the U.K. Biobank, some individuals walking among us have a natural loss-of-function mutation that disables the INHBE gene. That changes how their bodies metabolize lipids to provide protection against type 2 diabetes, heart disease, and obesity. Lucky bastards.

Importantly, this is a new mechanism of action. It doesn't impact appetite, reduce lean muscle mass, or trigger gastrointestinal side effects that lead half of all patients to discontinue GLP-1 use within the first year of treatment. Patients might only need two to four doses per year.

Wave Life Sciences teased super preliminary phase 1 data for its INHBE inhibitor, WVE-007, in December 2025. At the Week 12 check in, a single subcutaneous dose reduced visceral fat by 9.2%, total fat mass by 4.0%, and led to an increase of 0.9% in lean muscle mass. The company plans to explore combinations with other obesity treatments, including Wegovy from Novo Nordisk.

Arrowhead Pharmaceuticals followed with promising early data for two next-generation obesity candidates. At the Week 16 check in, a combination of ARO-INHBE and Zepbound from Eli Lilly doubled the weight loss of Zepbound alone in obese patients with type 2 diabetes. ARO-INHBE alone reduced visceral fat by 9.9% sixteen weeks after a single subcutaneous dose, while two doses led to a placebo-adjusted visceral fat reduction of 15.6% at Week 24. The monotherapy increased lean muscle mass by 3.6%.

Meanwhile, ARO-ALK7, the first RNAi drug candidate to target gene expression in fat tissues, achieved a 14.1% placebo-adjusted reduction in visceral fat eight weeks after a single subcutaneous dose. The ALK7 gene is downstream of INHBE and worth exploring as an alternative for competitive positioning.

There's a long way to go for INHBE and ALK7 drug candidates. Clinical trials for cardiometabolic studies will each require hundreds if not thousands of patients. Wave Life Sciences and Arrowhead Pharmaceuticals have disclosed data for less than 50 patients combined. Additionally, the mechanism of action has advantages but could potentially trigger ketoacidosis, which might be fatal for diabetes patients and dash development plans. No signs of serious ketoacidosis have been reported in preliminary data readouts.

Nonetheless, these assets could represent important new obesity treatments, including combinations and long-term maintenance therapy to keep the pounds off without the side effects. Combination treatments could reduce gastrointestinal side effects of existing GLP-1 drugs while preserving muscle mass. This could be achieved by reducing the required dose of GLP-1 drug, which would have the added benefit of increasing the value of existing manufacturing assets. That's potentially billions of dollars in additional value creation. Only Eli Lilly and Novo Nordisk can realize the benefit.

And yet.

Novo Nordisk Already Owns Its Future Growth Engine

Novo Nordisk acquired one of the leading RNAi technology platforms when it scooped up Dicerna Pharmaceuticals for $3.3 billion. But it has throttled the platform's contributions to two active clinical programs and a niche approval. That's it. The pharma leader hasn't developed internal assets for cardiometabolic disorders or obesity, let alone leverage internal capabilities to diversify away from those two increasingly crowded therapeutic areas.

It embarrassingly lost the bidding war for obesity drug developer Metsera to Pfizer, but was willing to pay up to $6.5 billion. Why not spend a fraction of those resources to bolster internal RNAi capabilities?

Then again, Novo Nordisk almost lost the acquisition bid for Dicerna years ago (to none other than Eli Lilly) and hasn't done much with the assets. Maybe Metsera is better off with Pfizer.

To be fair, the GalXC and GalXC Plus tools developed by Dicerna Pharmaceuticals weren't perfect. The company could deliver its RNAi payloads to the liver just like everyone else. Easy peasy. Selectively shuttling short-interfering RNA (siRNA) molecules to other tissue types is more challenging.

GalXC Plus planned to use lipids to get RNAi payloads into the proper cells. By engineering the length and side chains of a lipid, then slapping it onto the siRNA molecule that does all the gene silencing, Dicerna thought it could tune delivery to specific cell types. One configuration might shuttle payloads to fat tissues. Another could cross the blood-brain barrier. Less mature lipid ligands showed promise in delivery payloads to the liver and fat simultaneously. These tools were never clinically validated prior to the acquisition, but a similar approach was invented by researchers at UMass -- home to Dr. Mello, who won the 2006 Nobel Prize in Physiology or Medicine for the discovery of RNAi.

Being objective is important, especially if you want to consistently outperform as an investor. But shareholders should still consider Novo Nordisk's fumbling of the RNAi platform as malpractice.

Why doesn't Novo Nordisk have an internal INHBE program at the very least as one option in its next-gen pipeline? That doesn't require any new tissue targeting tools. It's losing the race to Wave Life Sciences and Arrowhead Pharmaceuticals, which each have solid technology platforms but command a fraction of the resources.

If Hong Chow wants to get moderately more ambitious, then there are low-hanging fruits adjacent to the obesity tree. For example, Novo Nordisk's promising oral NLRP3 inhibitor has broad potential against inflammatory conditions. It just so happens that NLRP3 is perched right between the inflammasome and complement-mediated complexes, two systems that determine how the immune system reacts to everything from blunt trauma to viruses to incorrectly attacking your own cells. Complement-mediated disorders are another perfect target for RNAi drug candidates, as evidenced by Arrowhead's promising data readouts to date. It doesn't require special delivery tools either.

Similar to next-generation obesity targets, this opportunity is sitting in plain sight. Eli Lilly just acquired Ventyx Biosciences for $1.2 billion to get ahold of its early-stage NLRP3 inhibitor. Meanwhile, complement-mediated disease specialist Alexion Pharmaceuticals was acquired by AstraZeneca for $39 billion in 2021. It was the fifth-largest biotech acquisition since 2018 and second-largest since the pandemic. Novo Nordisk has all of these pieces internally. It's simply chosen not to develop them intelligently.

Finally, if the business strategy team in Denmark wants to get a little more ambitious (admittedly difficult for the risk-averse Europeans), there are countless opportunities to develop RNAi assets for future growth potential. Novo Nordisk could develop drug candidates in new therapeutic areas that it only intends to partner to de-risk development. A similar strategy for neuro RNAi candidates has raked in over $1.3 billion in upfront cash for Arrowhead Pharmaceuticals. Most of the assets involved in licensing deals with Novartis and Sarepta Therapeutics hadn't even entered clinical trials yet.

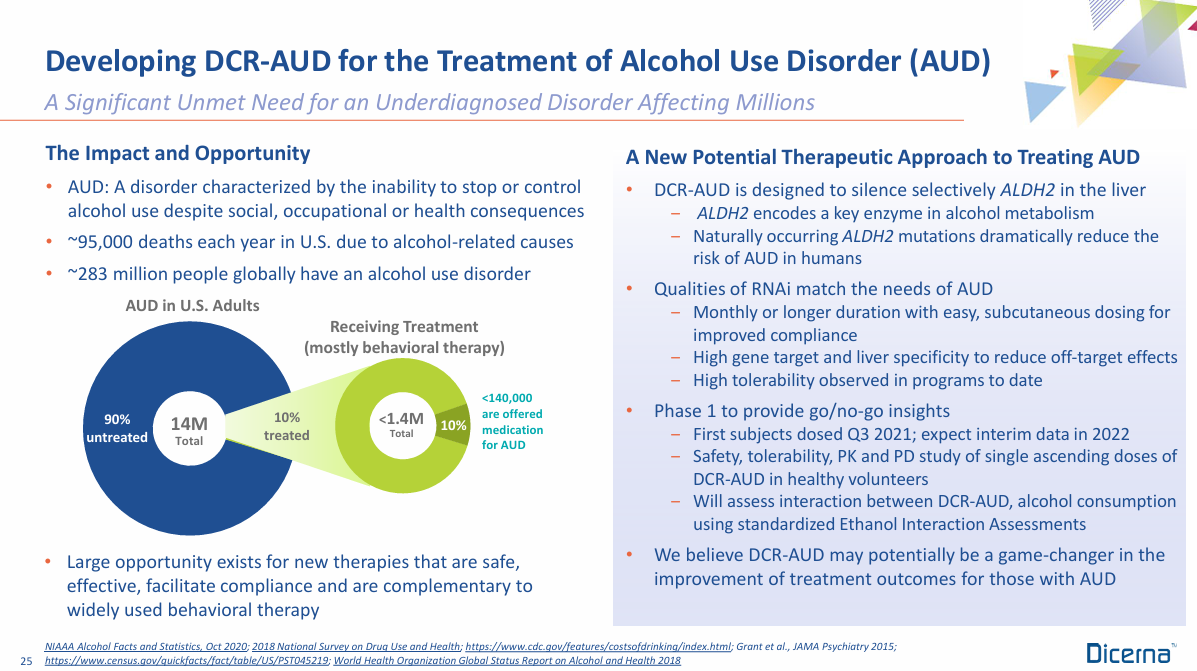

This could include a bet or two on ambitious programs that make most large pharma executives squirm. For example, Dicerna Pharmaceuticals was in the middle of a phase 1 study evaluating DCR-AUD for treating alcohol use disorder, also known as alcoholism. Once again, it was an opportunity uniquely suited for the therapeutic modality. And with an estimated global patient population of 283 million individuals, it's one of the few commercial opportunities that could rival obesity.

There is no competition.

When humans drink alcohol, they metabolize it into acetaldehyde. That's the molecule you can curse the next time you're hungover. Humans further metabolize toxic acetaldehyde into non-toxic acetate using enzymes encoded by the ALDH2 gene. Unfortunately, some individuals carry one or even two mutated copies of this gene that makes those enzymes less effective. Whether harboring one or two mutated copies, the result is the same: these individuals feel sicker after drinking relatively little alcohol because acetaldehyde isn't being cleared quickly enough. This is the nerdy, biochemical reason many individuals of Asian descent have low tolerance for alcohol. If that's you, then you have two copies of each gene, one from each parent. Pick at least one you want to blame.

RNAi drug developers have typically focused on genes like INHBE that are primarily expressed in the liver. If the liver was only responsible for 10% of your body's total INHBE output, then a liver-targeted RNAi drug candidate wouldn't be all that effective. However, scientists at Dicerna cleverly observed that roughly half of the body's ALDH2 gene expression occurs in the liver. In other words, an effective liver-directed gene silencer could recreate the natural genotypes of individuals with a single, disabled copy of the gene. In effect, it might be possible to use RNAi to temporarily make people not want to drink alcohol, allowing time to change behavior and treat alcohol use disorder. All with two to four doses per year and no meaningful competition.

Novo Nordisk terminated DCR-AUD without sharing data. Maybe the initial results disproved the clinical hypothesis. Maybe the commercial opportunity was considered riskier to develop (it was going to be a heavy lift for tiny Dicerna). But maybe the old management team was so fixated on peptides and obesity and obesity and obesity that it exercised poor judgement in portfolio decisions.

With or without ambitious "white space" opportunities like DCR-AUD, executives have never offered a great reason for essentially idling its RNAi tools. The genetic medicine platform -- and all the intellectual property it contained -- could be generating considerable value for Novo Nordisk while positively changing the investment narrative. It's not too late to start.

Disclosure: I have no investment positions in any companies mentioned in this article.

Yes, biotech stocks can beat the market.

Solt DB is a biotech equities research firm. We manage a real-money, long-term oriented, 100% transparent investment portfolio called Finch Trades. As of June 30, 2026 (updated quarterly), we're outperforming the S&P 500 by 97.7%, Nasdaq 100 by 83.7%, XBI by 60.5%, and Ark Genomic Revolution ETF by 64.4%.

Memberships to investment research fund our mission as a public benefit company and keep us fiercely independent – so we can keep giving tech bros the bird. No ads, no clickbait, no hype. Join today for $26.25 per month.

.svg)

.avif)

.svg)

.svg)

%20(squoosh).jpg)

%20(squoosh).jpg)

%20(thumbnail)%20(squoosh).jpg)

.svg)

.svg)

.svg)